Accounting is a complex and detail-oriented field that demands precision and accuracy. While many associate accounting primarily with numbers and financial statements, effective time management is one of the most critical aspects of the profession. In the accounting world, time is money, and how it’s managed can significantly impact the quality of work, client satisfaction, and even the financial health of a business.

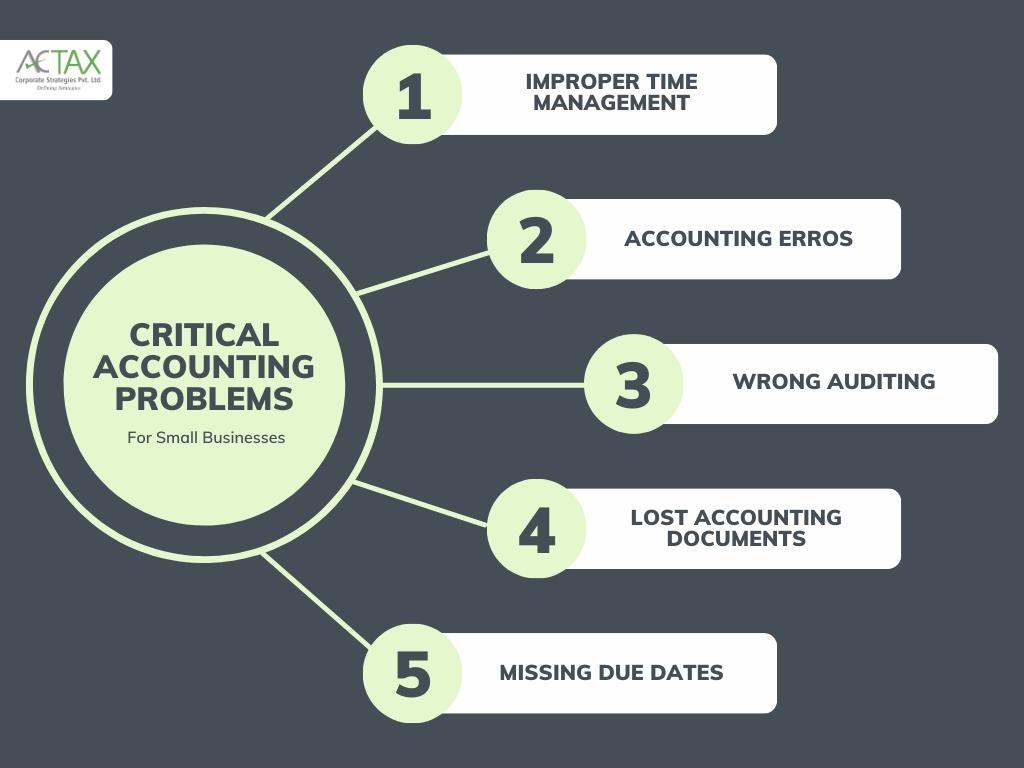

Why Time Management is a Critical Problem with Accounting?

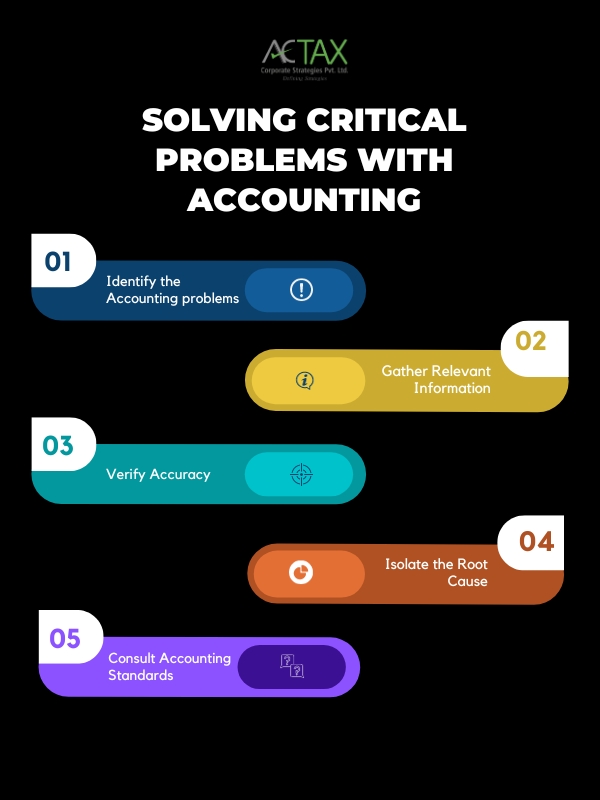

Improper time management can be the biggest problem with your accounting system. A simple idea to overcome is only with proper training on the importance of Time & impact of timeliness on accounting process.

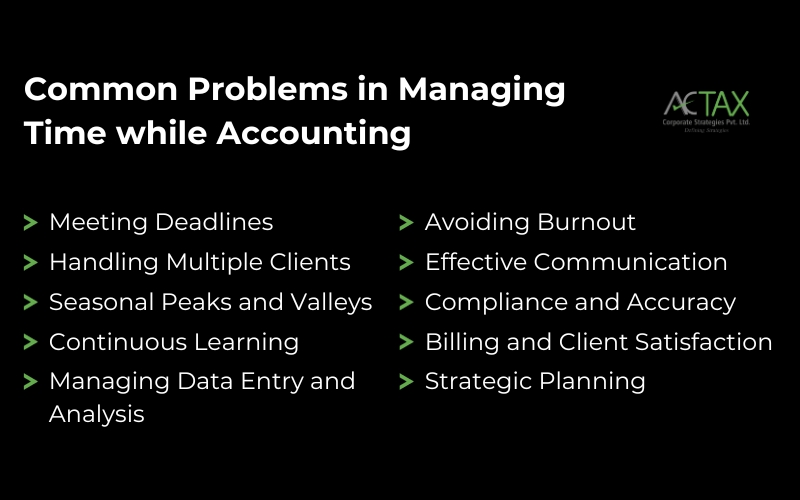

1. Meeting Deadlines

One of the fundamental responsibilities of accountants is to meet deadlines for financial reporting, tax filings, and audits. Please meet these deadlines to avoid penalties, legal issues, and a loss of credibility. Effective time management is crucial to ensure all necessary tasks are completed promptly

2. Handling Multiple Clients

Many accountants work with multiple clients simultaneously, each with unique accounting needs. Juggling these diverse requirements, tracking deadlines, and maintaining accuracy can be overwhelming without efficient time management strategies. Accountants need to allocate their time effectively to serve all clients adequately.

3. Seasonal Peaks and Valleys

Accounting experiences seasonal variations in workload, especially during tax season or year-end reporting. During these peaks, time management becomes even more critical. Accountants must efficiently allocate time to handle the increased workload without compromising accuracy.

4. Continuous Learning

The accounting field is subject to ever-evolving regulations and technologies. Accountants must invest time in continuous learning to stay updated and maintain professional competence. Managing ongoing education and training time is essential to keep up with industry changes.

5. Managing Data Entry and Analysis

Much accounting work involves data entry and analysis. Efficiently managing the time spent on these tasks is vital for maintaining accuracy while minimizing the risk of errors. Automating repetitive tasks can free up time for more critical analytical work.

6. Avoiding Burnout

Poor time management can lead to overwork and burnout. Accountants often face high-pressure situations; failing to manage their time effectively can result in long hours and high-stress levels. Burnout can have severe physical and mental health implications.

7. Effective Communication

Time management extends beyond individual tasks. Accountants must also manage their time for effective communication with clients, colleagues, and regulatory authorities. Delayed responses and missed meetings can harm professional relationships.

8. Compliance and Accuracy

Rushing through tasks due to poor time management can compromise the accuracy and quality of accounting work. This can result in errors in financial statements, audits, and tax filings, potentially leading to legal consequences.

9. Billing and Client Satisfaction

Accountants often bill clients based on billable hours. Effective time management not only ensures accurate billing but also influences client satisfaction. Clients value efficient and timely service.

10. Strategic Planning

Beyond the day-to-day tasks, accountants are often involved in strategic financial planning for their clients or organizations. Allocating time for long-term financial strategies and forecasts is essential for success.

{kind=link}

Pingback: Accounting principles for Small Businesses | Actax India

Pingback: 8 Best Cloud Accounting Software in India for 2024 | Actax India

Pingback: 6 AI Tools for Accounting in India: Unveiling Secrets | Actax India