Accounting is changing, accountants are evolving, the true question lies in – Are businesses adopting new accounting principles?

Gone those days of traditional bookkeeping & accounting practices. Now, accounting runs on traditional principles with modern & tech-enabled execution. With AI integration in accounting & bookkeeping, accounting principles are evolving year on year.

We have observed huge changes in accounting practices & usage of technology in Real-time accounting & how they are benefiting business owners to make progress. So, we are updating this article on basic principles of accounting with evolving principles, not only guiding the accountants but helping novice & growing founders to incorporate them for business success.

Summarize Full Article Quickly

1. The Core Evolution: From History to Real-Time

The traditional “Generally Accepted Accounting Principles” (GAAP) are no longer just static rules; they are now embedded into automated systems.

- Traditional Accounting: Relied on month-end reports and manual entry.

- 2026 Accounting: Utilizes AI and live dashboards to provide founders with immediate insights for agile decision-making.

2. The 5 Evolving Principles (Updated for 2026)

| Principle | Traditional Definition | 2026 Modern Insight |

| Revenue Recognition | Record when earned/realized. | Crucial for SaaS/Subscription models to track deferred revenue accurately. |

| Cost Principle | Assets recorded at historical purchase price. | Now supported by AI-driven live tracking and verifiable digital data. |

| Matching Principle | Expenses must match revenue periods. | Renamed as the “Principle of Real-Time Intelligence” due to instant auto-reconciliation. |

| Full Disclosure | Provide all relevant financial info. | Now includes Non-Financial Data like Carbon Footprints and ESG (Energy Efficiency) scores. |

| Objectivity Principle | Information must be factual/unbiased. | Ensured through automated audit trails that eliminate human error and personal bias. |

3. Strategic Benefits for Small Businesses

Adopting these updated principles offers four primary advantages:

- Credibility: High-quality, transparent reporting attracts investors and secures bank loans.

- Informed Growth: Real-time data allows founders to pivot strategies mid-month rather than waiting for quarterly reviews.

- Compliance: Automatic alignment with GST, IFRS, and tax laws reduces legal risks.

- Efficiency: AI integration makes audits faster and less stressful.

4. Addressing the Limitations

The article honestly acknowledges that modernizing accounting isn’t without hurdles:

- Complexity: New standards require a learning curve for novice founders.

- Cost: Initial investment in specialized software or expert consultants can be high.

- Rigidity: Standardized rules can sometimes feel ill-fitted for unique, niche business models.

The “New Perspective” Takeaway

The most significant insight is that accounting is no longer a “cost center” for compliance; it is a “growth engine” for strategy. By integrating AI and ESG metrics into these five principles, businesses gain a “Financial GPS” that prevents them from “driving off a cliff” while navigating the complex market of 2026.

Introduction to Accounting Principles With Need of Understanding Them

Accounting principles, also known as Generally Accepted Accounting Principles (GAAP), are standardized guidelines and rules governing financial accounting and reporting, alongside 3 golden rules of accounting.

These principles ensure consistency, transparency, and accuracy in financial statements and transactions. Fundamental principles include the accrual basis, which records transactions when they occur rather than when cash changes hands, and the principle of materiality, which focuses on reporting significant financial information.

Adhering to these principles enables businesses and organizations to prepare financial statements that provide an accurate and fair view of their financial health, facilitating informed decision-making and regulatory compliance. Now it is time to incorporate new accounting principles which are essentially important with the intervention of AI.

Why Accountants & Businesses Should Follow Accounting Principles?

Accounting principles are crucial for several reasons –

- They provide a standardized framework for recording and reporting financial transactions, ensuring consistency and comparability across different businesses. This enables stakeholders to assess and analyze financial information accurately.

- It promotes transparency, which builds trust among investors, creditors, and other interested parties.

- These principles help in making informed business decisions, as they provide reliable and relevant financial data.

- Following accounting principles is often a legal requirement, ensuring compliance with regulatory standards and avoiding legal issues.

Overall, these principles are essential for maintaining the integrity and reliability of financial reporting in any organization.

Do Small Businesses Follow Accounting Principles?

Yes, small businesses should follow accounting principles. Adhering to these principles ensures accurate financial records, facilitates informed decision-making, and builds credibility with stakeholders. It also helps small companies meet legal and regulatory requirements, paving the way for sustainable growth and financial stability.

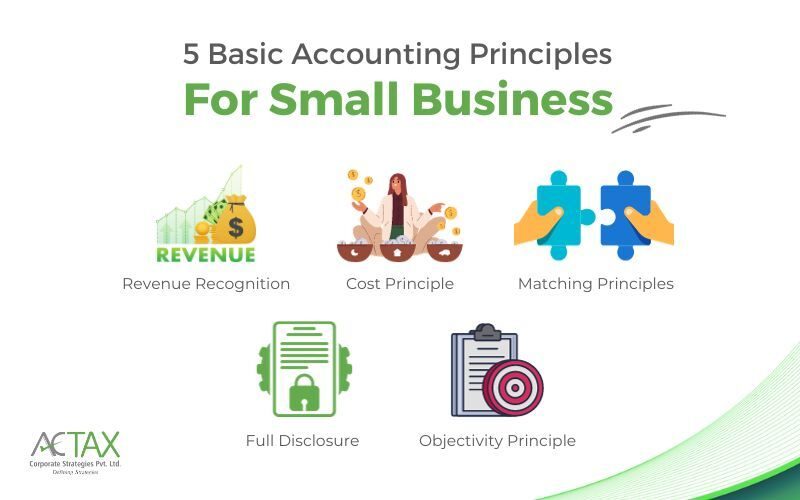

Here Are 5 Key Accounting Principles All Businesses Should Follow

Principle of Revenue Recognition & Its Elements

The Revenue Recognition Principle is a fundamental accounting principle that guides how businesses record their revenue in financial statements. Maintaining accurate financial reporting, making informed decisions, and assessing a company’s financial health are crucial.

Here’s a comprehensive explanation of the Revenue Recognition Accounting Principle elements:

1. Earning Revenue

To recognize revenue, a business must have fulfilled its obligations, often delivering goods or services to the customer. The payment is considered “earned” when this occurs.

2. Realization

Revenue is recognized when it is “realized,” or it becomes clear that the company will receive payment for the goods or services. This usually happens when a sales transaction occurs, and a legally binding agreement is in place.

3. Accurate Financial Statements

Adhering to the Revenue Recognition Principle ensures that a company’s financial statements accurately reflect its financial performance. This transparency is vital for stakeholders, including investors, creditors, and management, to assess the company’s profitability and financial health.

4. Consistency

This principle promotes feeling in revenue reporting across accounting periods, making comparing financial statements from different periods easier. Consistency is essential for trend analysis and decision-making.

5. Legal And Regulatory Compliance

Many accounting standards, such as the Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), require businesses to follow the Revenue Recognition Principle. Compliance with these standards is often a legal requirement for publicly traded companies.

Accounting Principle 2: The Cost Principle

The cost principle emphasizes historical cost, meaning that accounting records should reflect the actual amounts paid when transactions occur. This cost accounting principle promotes using objective and verifiable data, making tracking and comparing financial data more accessible over time.

Conservatism

The cost principle aligns with the conservative approach in accounting, which is the principle of erring on the side of caution. Recording assets at their original cost helps avoid overstatement of asset values, ensuring that financial statements are balanced.

Comparability

Historical cost allows for consistency and comparability in financial reporting. When all businesses record their assets and liabilities at their original prices, it becomes easier to compare the financial statements of different entities and assess their relative financial health and performance.

Objective Measurement

The cost principle provides an accurate and reliable basis for measuring financial transactions. Unlike subjective valuations, such as fair value, historical cost is typically based on actual transactions, invoices, and receipts.

Valuation Over Time

While the cost principle dictates the initial recording of assets and liabilities, it is essential to note that specific assets may be subject to impairment charges if their carrying value exceeds their recoverable amount after their initial recognition. However, this does not alter the cost principle governing initial valuation.

What Is Changing in the Cost Principle Concept in 2026?

The cost principle concept, also known as the historical cost principle, is one of the fundamental principles that serves as a foundational concept in financial reporting. It is one of several principles of accounting that guide accountants in preparing financial statements and reports that accurately reflect a company’s financial position and performance.

In 2026, with the enhanced capability of AI reporting transactions & performing bookkeeping efficiently, the live dashboards are replacing traditional accounting methods. Now, founders can make decisions with the real-time accounting data & financial reports. You don’t have to wait for a month-end or a year to analyse the business performance.

The cost principle is essential for ensuring the reliability, consistency, and comparability.

Accounting Principle 3: The Matching Accounting Principles

The matching principle, also known as the expense recognition principle, is one of the fundamental accounting principles. It plays a crucial role in the accrual basis of accounting, which is widely used in financial reporting. The matching principle guides accountants in determining when and how to recognize expenses in the income statement.

The matching principle ensures a clear cause-and-effect relationship between expenses and the revenues they help generate. This means that expenses are recognized in the same period as the associated revenues to portray a company’s profitability accurately.

Now, accounting has evolved with real-time accounting insights offering live dashboard data with income-expenses matching as and when the transactions are recorded. Our Actax accounting experts have renamed it as “Principle of Real Time Intelligence”.

1. Accrual Basis Accounting

The matching accounting principle is a fundamental component of accrual basis accounting, which is the preferred accounting method for most businesses. Accrual accounting recognizes revenues when earned and expenses when incurred rather than when cash is exchanged.

2. Periodicity

Following the matching principle, financial statements are prepared periodically (e.g., monthly, quarterly, or annually). This allows stakeholders to assess a business’s financial performance and profitability during specific periods.

3. Consistency And Comparability

Consistently applying the matching principle ensures that financial statements are comparable from one accounting period to another. This comparability aids investors, creditors, and analysts in making informed decisions.

4. Income Smoothing

The matching principle discourages manipulating financial results by artificially delaying the recognition of expenses or prepaying expenses to boost short-term profitability. It promotes a more realistic and sustainable representation of financial performance.

Accounting Principle 4: Full Disclosure Accounting Principle

The full disclosure principle, also known as the disclosure principle, is a fundamental accounting and financial reporting principle. This principle emphasizes the importance of providing complete and transparent information in financial statements and related disclosures to ensure that users can access all relevant information to make informed decisions.

The full disclosure principle promotes transparency in financial reporting. It ensures that stakeholders, including investors, creditors, regulators, and analysts, have access to all essential information about a company’s financial activities, risks, and significant events.

What’s New in the Principle of Full Disclosure in 2026?

In recent times, the accounting reports must also include non-financial data, like the Materiality of Impact. Tracking the carbon footprints also matters most now. In modern accounting, this new principle must be included to secure funding & loans from banks. This precisely shows the data of your business contribution to energy efficiency & social impact along with your P&L.

Now, you will understand why Brands like Samsung, Sony, LG, etc., put a rating badge of energy savings on all the appliances.

It Offers Complete Information

Financial statements alone may not provide a comprehensive picture of a company’s financial health and operations. Disclosures, such as footnotes, management’s discussion and analysis (MD&A), carbon footprints, and supplementary schedules, provide additional context and detail.

Materiality

This principle recognizes that not all information is equally significant. Disclosures should focus on material information that could influence users’ decisions. Materiality is determined by factors such as the dollar amount, the nature of the item, and the potential impact on financial statement users.

Consistency

The full disclosure principle encourages consistency in reporting. Companies should consistently disclose similar types of information and use standard formats and terminology to make it easier for users to compare financial information across different periods and entities.

Legal And Regulatory Requirements

Many jurisdictions have legal and regulatory requirements that mandate specific disclosures. Adhering to these requirements helps companies avoid legal and compliance issues.

Accounting Principle 5: Objectivity Principle

The objectivity principle, also known as the objectivity concept or the impartiality principle, is one of the fundamental principles of financial accounting.

It plays a crucial role in maintaining the integrity and credibility of financial reporting. This principle emphasizes the importance of presenting financial information as unbiased, factual, and verifiable, free from personal biases or opinions.

Unbiased Reporting

The objectivity accounting principles ensure that financial reporting is free from undue bias or subjectivity. Financial professionals must maintain a neutral and impartial stance when recording and reporting financial transactions.

Credibility And Reliability

Objective financial information is more credible and reliable because it is based on verifiable evidence. This credibility is essential for gaining the trust of stakeholders, including investors, creditors, regulators, and the public.

Consistency

Consistent application of objective accounting standards and principles of financial accounting across different periods and entities enhances comparability and allows users to make meaningful comparisons.

Auditability

The objectivity principle facilitates the auditing process. Auditors can review financial transactions and verify the accuracy and reliability of reported information when it is based on objective evidence.

Avoidance Of Bias

Personal biases or opinions can lead to financial reporting that is overly optimistic or pessimistic. The objectivity principle helps eliminate these biases, promoting more accurate financial statements.

What Are The Benefits of Following Accounting Principles for Small Businesses?

Accounting principle offers several significant benefits for small businesses

1. Accuracy And Consistency

Following accounting principles ensures that financial transactions are recorded consistently and accurately. This consistency makes it easier to track income, expenses, and assets over time, reducing the likelihood of errors that could lead to financial discrepancies.

2. Informed Decision-Making

Small business owners rely on financial information to make critical decisions. Adhering to accounting principles provides reliable data, enabling informed choices about investments, cost-cutting measures, pricing strategies, and expansion opportunities.

3. Credibility And Trust

Consistent financial reporting based on accounting principles builds trust with stakeholders, including investors, lenders, customers, and suppliers. Credibility can lead to increased access to financing and stronger business relationships.

4. Legal And Regulatory Compliance

Many jurisdictions require businesses to follow specific tax reporting and regulatory compliance accounting principles. Adhering to these principles helps small businesses avoid legal issues, penalties, and fines.

5. Easier Auditing And Financial Reviews

When small businesses maintain accurate and consistent financial records based on accounting principles, audits and financial reviews become more straightforward and less time-consuming. This reduces the cost and stress associated with regulatory inspections.

What Are The Limitations of Accounting Principles to Small Businesses?

While accounting principle offers numerous benefits to small businesses, they also come with certain limitations

1. Increases Complexity

Accounting principles can be intricate and challenging to implement correctly, especially for small businesses with limited financial expertise. This complexity can result in errors or misinterpretations, leading to inaccurate financial reporting.

2. Comes With Resource Constraints

Small businesses often need more resources and personnel to fully comply with complex accounting standards. Hiring specialized accountants or investing in cloud-based accounting software can strain limited budgets.

3. Its is Time-Consuming with Alternatives

Maintaining meticulous financial records according to accounting principles can be time-consuming for small business owners juggling multiple responsibilities. This can divert their focus from core operations.

4. Incurs Additional Costs

Adhering to accounting principles may involve additional costs, such as software licenses, training, or hiring experts. Small businesses may need help to justify these expenses, particularly if they need more financial resources.

5. Very Rigid Standards To Follow

Accounting principles are designed to be applicable across various industries and businesses. However, they may only sometimes align perfectly with small businesses’ unique needs and nuances, leading to unnecessary complexity.

Take Aways from Accounting Principles

In conclusion, the five basic accounting principles, namely, the Revenue Recognition Principle, Expense Recognition (Matching) Principle, Historical Cost (Cost) Principle, Full Disclosure Principle, and Objectivity Principle, together form the foundational framework that guides the practice of accounting and financial reporting.

With technology, some industry limitations are expanded & growing beyond the boundaries, creating a way for limitless performance. The accounting field is also getting impacted by new-age accounting methods. Hence, accounting principles aren’t a cage that restricts your business, but a GPS that ensures you don’t drive off a cliff.

{kind=link}

Comments are closed.